4,904 strategies. 102 made money. The play that won last week is dead.

Not investment advice. Educational content only. Results are from a backtest, not live trading. Full disclaimer at the end.

Over the last week we generated 4,904 distinct trading strategies, fed them into Turbine's backtest engine, and ran every one of them against Kalshi's 15-minute BTC market series (KXBTC15M) over the last 30 days. Each strategy executes across roughly 2,831 individual markets in the window. That is 13.9 million simulated strategy-market pairings, 41.8 million simulated trades.

This is the second run we have done on this series. The first one last week told a story: most strategies made money, the simple "buy cheap, sell on bounce" idea was the winner, and the leaderboard was full of it. Since then, we incorporated feedback from this subreddit to make the backtesting more accurate:

- Liquidity consideration

- Fees considerations

- Taking the next candle open instead of the current 1m candle

The Headline

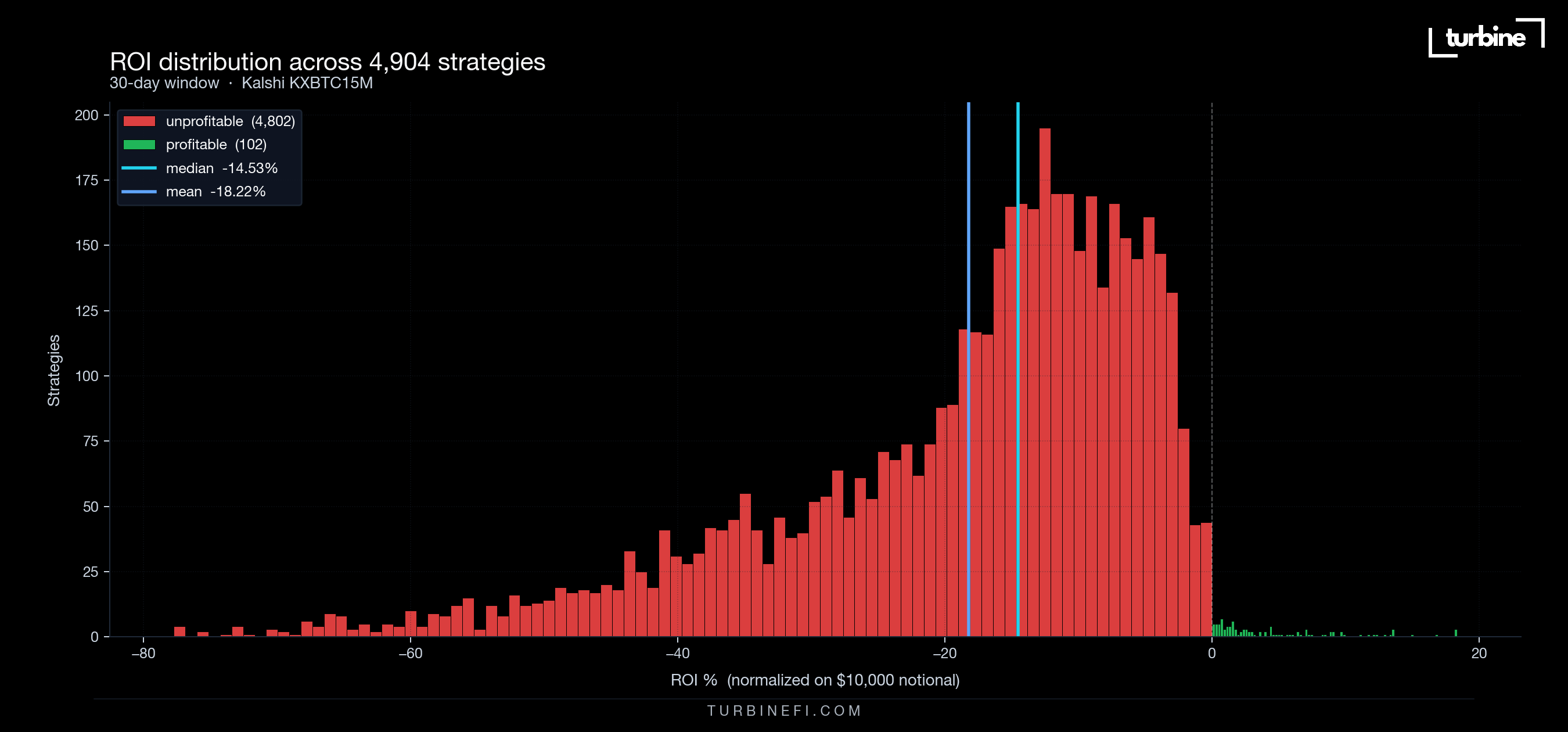

Out of 4,904 strategies, 102 made money. 4,802 did not. Median ROI was -14.53% on a $10,000 notional. The best strategy returned +18.32%. The worst returned -77.73%.

This is a one-sided distribution. There is no heavy right tail. There is one tight cluster of winners at the top, and a giant red wall everywhere else.

The Zero-for-432 Loser

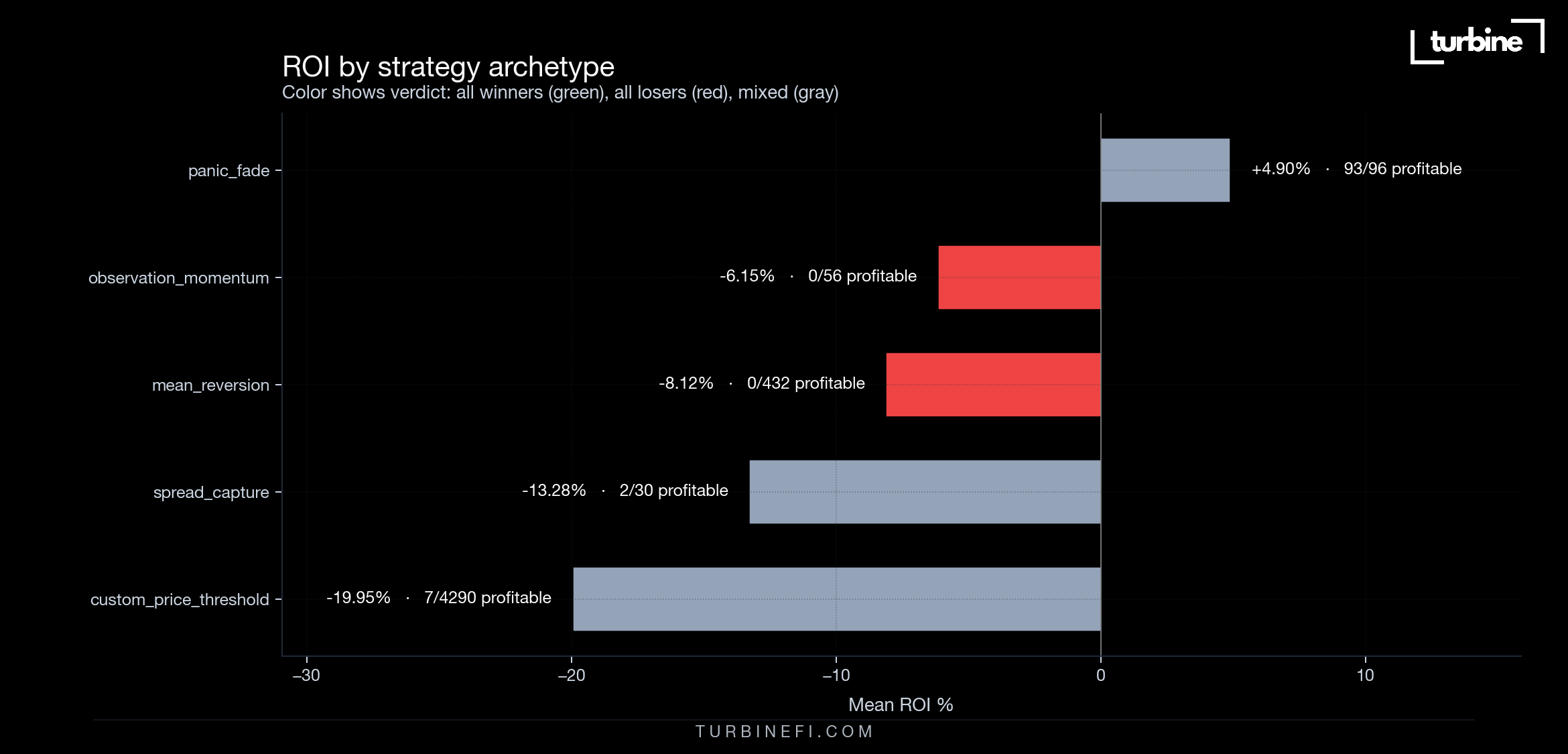

mean_reversion was 0 for 432. Not a single variant made money. We tested entry bands from 0.10 to 0.40 against exits at 0.50 to 0.90, with cooldowns up to 30 minutes. Mean ROI -8.12%. Best variant -1.29%. Worst -14.26%.

The structural reason is duration. mean_reversion is a strategy that needs the price to drift away and come back inside the window the trader is waiting on it. On a 15-minute market, the price does not have time to do that. By the time the entry band fires, the market is closing. There is no reversion left to capture.

This is the same template that prints money on long-duration two-way books, NFL spreads, election markets that sit open for months. It does not work on 15-minute crypto. The duration eats it.

The 93-of-96 Winner (the only one that worked)

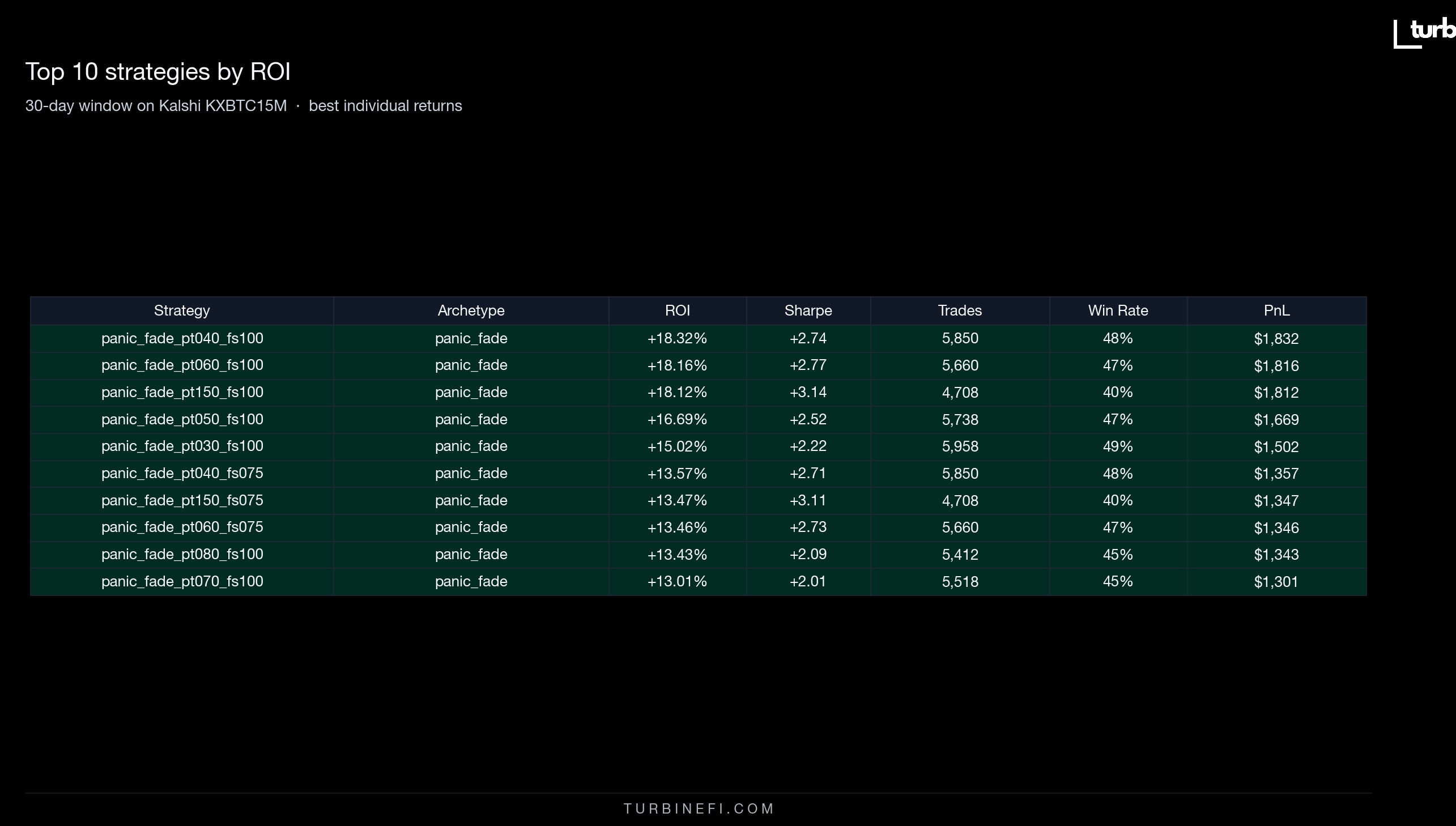

panic_fade was 93 of 96 profitable. Mean ROI +4.90%. The 3 losers all came in at -0.12%. Best variant +18.32%, on panic_threshold=0.04 with fade_size=100.

This is the only archetype on the leaderboard. Of the top 100 strategies in the entire run, 93 are panic_fade variants. The remaining 7 are custom price-threshold variants that barely cleared zero.

What works on KXBTC15M right now is volatility-reversion. When the book moves hard in 15 minutes, take the other side. Every parameterization of that idea pays. Everything else loses.

The Top 10 Were All the Same Parameter

Look at the top of the leaderboard:

Every one is panic_fade. Every one used fade_size=100. The panic_threshold ranges from 0.03 to 0.15, and it does not seem to matter much. What matters is size.

Pulling 100 contracts every time the book panics outperformed pulling 75 outperformed pulling 50. The smaller fade sizes printed too, just less. The pattern is unambiguous: in this regime, fade with conviction or do not fade at all.

The Trap That Was Last Week's Winner

Last week's research run on this same series had custom price-threshold strategies (buy YES at price X, sell at price Y) at the top of the leaderboard. The single best strategy was buy at 0.50, sell at 0.70. It returned +56.6% on a 30-day window ending 2026-04-20.

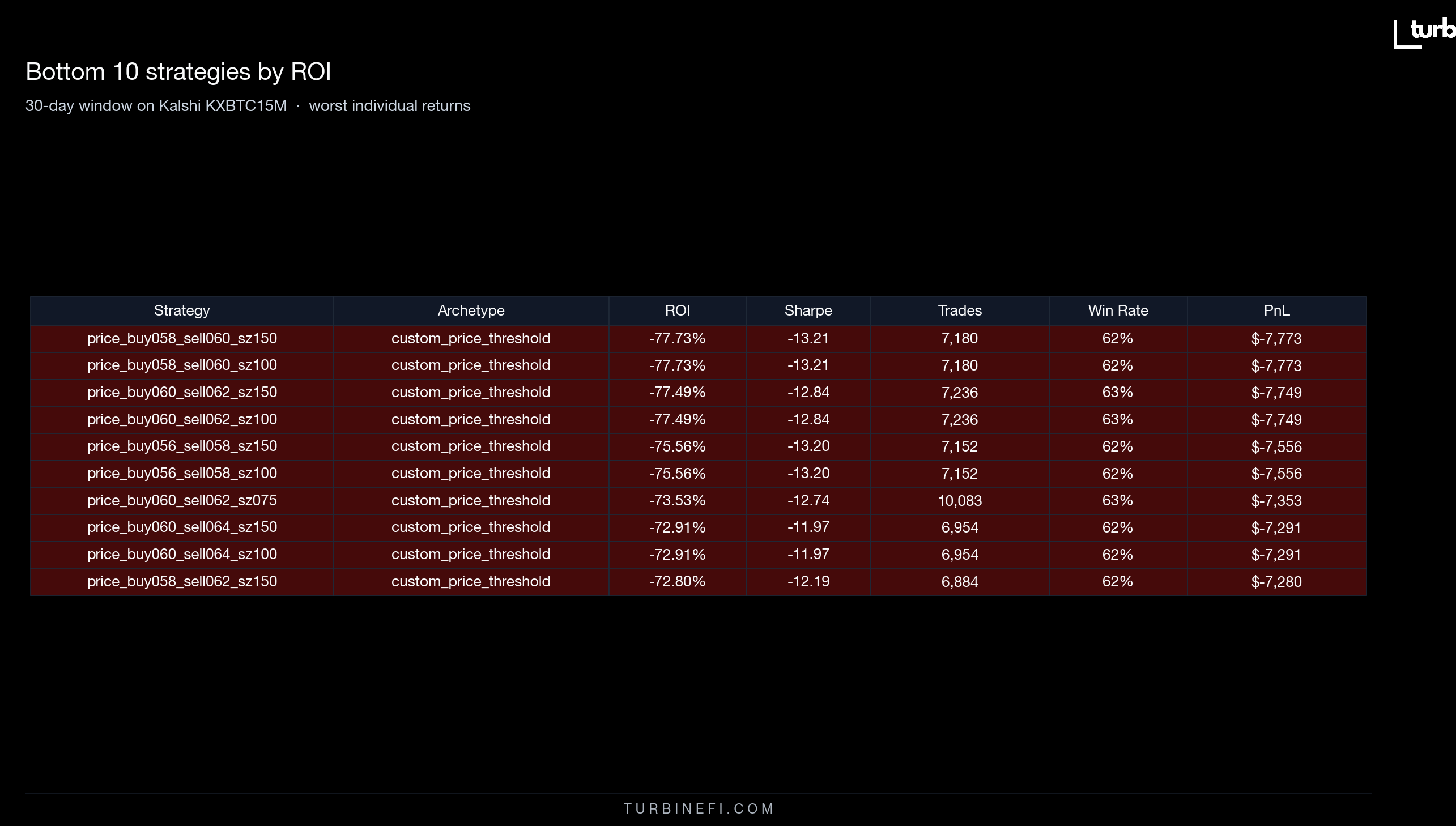

This run, with a 30-day window ending 2026-04-29, the same archetype is 7 of 4,290. 0.16% hit rate. Mean ROI -19.95%. Worst variant -77.73%.

That is the same idea, the same tickers, the same engine. Nine days of fresh data shifted in, nine old days shifted out, and the play that produced the inaugural leaderboard is now the worst-performing archetype by sample size in the run.

The bottom 10 strategies in this run are all tight-band price-threshold variants. buy 0.58, sell 0.60. buy 0.60, sell 0.62. 7,000+ trades each, 62-63% win rate, and still losing 75-78% over the window. They are being eaten alive by fees and slippage on a 2-cent target. When the book stops obediently mean-reverting, every one of those small wins becomes a small loss, and the cumulative bill is brutal.

The Bottom Line

- On KXBTC15M right now, fade the panic. It is the only thing that works.

- Size matters more than threshold. fade_size=100 dominated.

- Do not buy cheap and wait for the bounce. The bounce is not coming back fast enough on a 15-min market.

- Do not run a tight 2-cent price target with high turnover. Fees and slippage will eat you alive.

- Strategies are regime-dependent. The play that worked three weeks ago is now the worst archetype in the lab.

How We Ran It

All 4,904 strategies were generated deterministically from a parameter sweep, submitted to the production Turbine backtest API, and pulled back as a flat results file. Total wall time: 58 minutes for 41.8 million trades, on a 4-worker batch runner. You can browse the strategies and the underlying execution model in the Turbine Studio strategies tab under crypto.

If you want to run your own version of this, swap the series, change the window, try different archetypes. Turbine Studio lets you do it without writing code. Describe the strategy in plain English, we compile it to DSL, run the backtest, and give you the results.

We will keep doing these. Next run is probably ETH 15-min on the same shape, plus a couple of strategy ideas from comments. Reply with one and we will add it to the batch.

Follow @turbinefi for the next drop.

Caveats

One window (30 days, ending 2026-04-29), one series (KXBTC15M). Different window or series would produce a completely different leaderboard, and the contrast with our inaugural post on the same series proves it. Treat the shape of the findings as more durable than any individual rank.

ROI is normalized on a $10,000 notional because backtest equity curves are easier to compare that way. Relative ordering is accurate, read the percentages as "P&L per $10k deployed."

Backtests use historical orderbook snapshots. Live execution hits slippage, venue hiccups, and liquidity that moves under you. Past performance, hypothetical or real, does not predict future performance. The fact that the same archetypes that won three weeks ago are losing now is the cleanest demonstration of that you are likely to see.

Disclaimer

This post is for informational and educational purposes only. It is not investment advice, a recommendation to trade, or a solicitation to buy or sell any financial product, contract, or instrument. Turbine is not a registered investment adviser, broker-dealer, commodity trading advisor, or commodity pool operator.

The results described are from a backtest: a simulation of how strategies would have performed against historical orderbook data over a specific window on a single market series. Kalshi contracts are regulated by the U.S. Commodity Futures Trading Commission.

Hypothetical and simulated performance results have inherent limitations. They are prepared with the benefit of hindsight, do not involve real capital at risk, and cannot fully account for the impact of execution, liquidity, fees, or changes in market conditions. No representation is being made that any strategy will or is likely to achieve profits or losses similar to those shown.

Past performance, whether actual or hypothetical, is not indicative of future results. Trading prediction-market contracts involves substantial risk, including the possible loss of the entire amount invested.

Strategies described here were built and backtested by the author for research. Turbine does not recommend any of these strategies for use.

You are solely responsible for any decisions you make. Before trading any product, consider your financial situation and risk tolerance, and consult a qualified professional. Do not rely on anything in this post as the basis for a trading decision.