Does Coinbase Spot Lead Kalshi BTC? We Tested 100 Strategies.

Not investment advice. Educational backtest only. Results are from a backtest, not live trading. Full disclaimer at the end.

We ran 100 different Kalshi BTC 15-minute strategies through Turbine's backtest engine, but with one twist: every strategy used Coinbase BTC-USD data as an external signal.

The question was simple: if Kalshi is trading a short-duration BTC contract, does watching the underlying venue directly create edge?

In this one window, the data suggests yes.

Two weeks ago, panic fading dominated. Five days ago, almost nothing worked. In this run, using an external venue flips the result again: momentum, not reversion, wins.

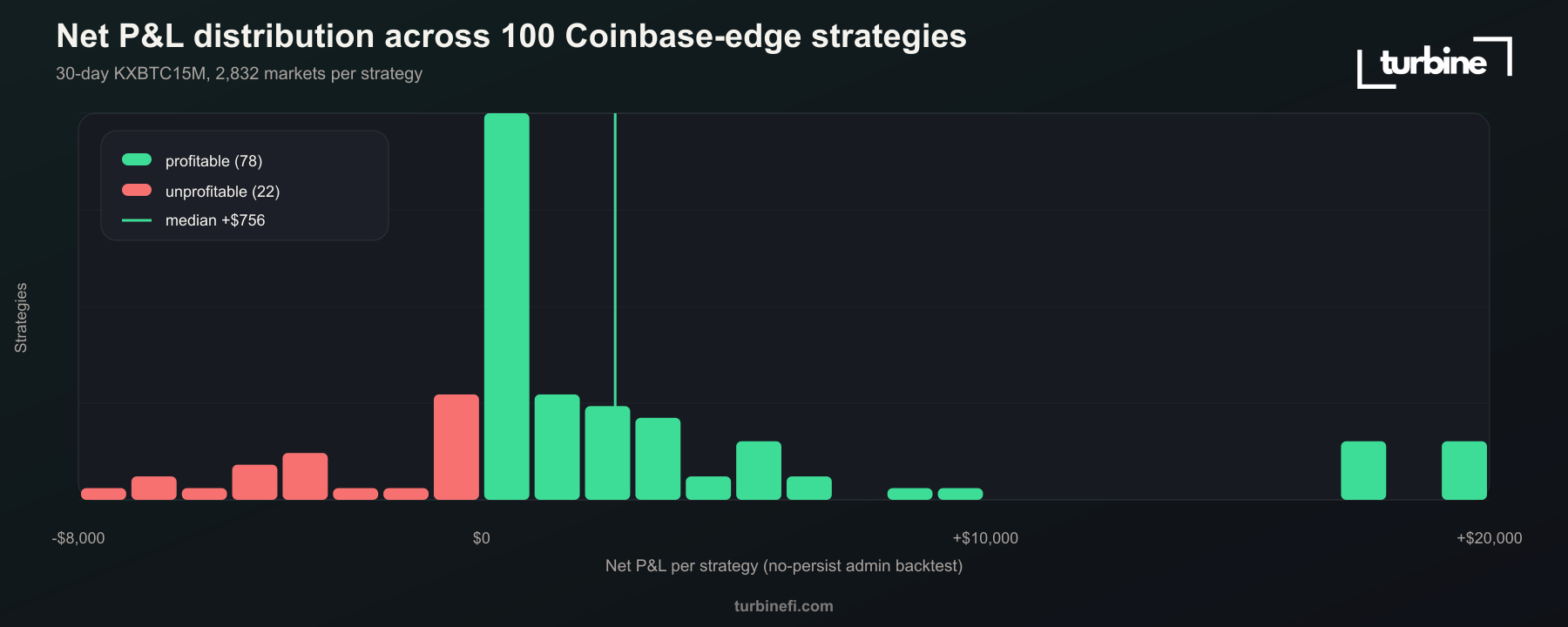

100 strategies. 78 made money. 22 lost.

- Window: 30 days, ending May 4, 2026

- Market series: KXBTC15M

- Markets simulated per strategy: 2,832

- Total simulated trades: 317,645

The best strategy made +$19,451. The worst lost -$7,278.

The headline: the best strategies did not fade Coinbase moves. They followed them.

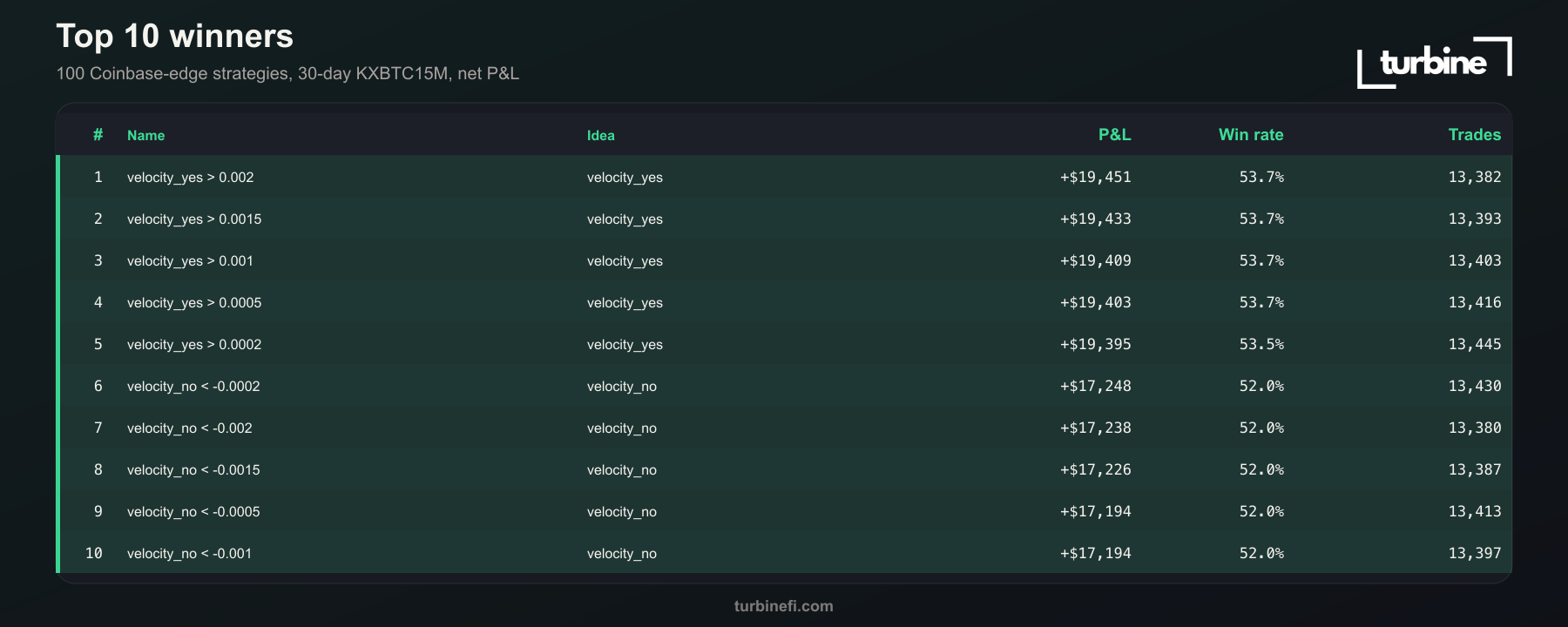

The Winner: Coinbase Velocity

The top 10 strategies were all 1-minute Coinbase velocity strategies.

Best strategy:

Buy YES when Coinbase BTC 1-minute velocity is positive above 0.002.

- Net simulated P&L: +$19,451

- Trades: 13,382

- Win rate: 53.74%

- Modeled fees paid: $4,412

The top five were all YES velocity variants. The threshold barely mattered. Whether the trigger was 0.0002 or 0.002, the result was basically the same. The edge was not "find the perfect velocity cutoff." The edge was "when Coinbase spot is moving up right now, Kalshi's 15-minute BTC contract still has enough lag to buy YES."

The NO side worked too. The five negative-velocity NO strategies averaged +$17,220 each.

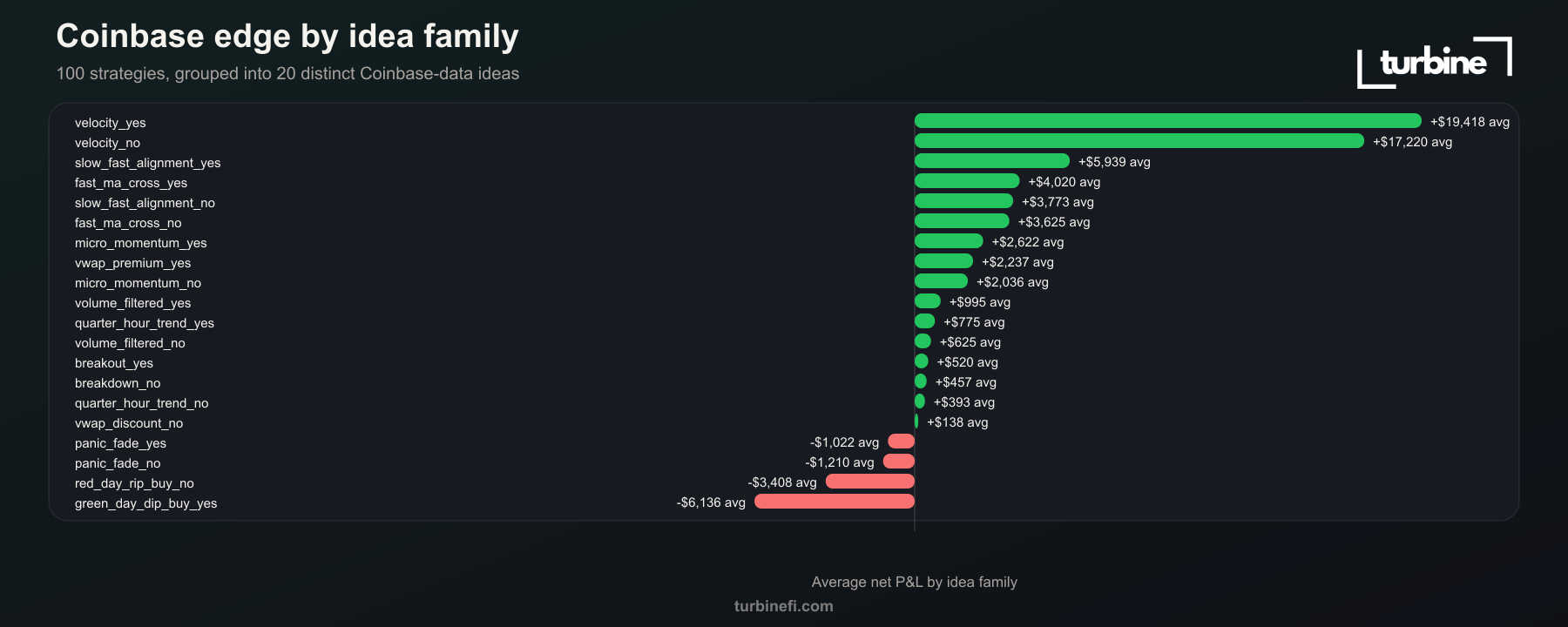

Second Best: Trend Alignment

Strategies that required Coinbase 1-hour and 5-minute trend to agree were all profitable.

- YES alignment: 5 of 5 profitable, mean P&L +$5,939

- NO alignment: 5 of 5 profitable, mean P&L +$3,773

This was less explosive than 1-minute velocity, but probably more interpretable. When Coinbase BTC was moving in the same direction across short and medium windows, Kalshi's 15-minute contract still had room to reprice.

Fast moving-average crossover worked too. YES strategies using fast EMA over short SMA were 5 of 5 profitable, with mean P&L +$4,020. NO strategies using the inverse setup were also 5 of 5 profitable, with mean P&L +$3,625.

The Full Breakdown

The strongest families were all momentum or trend-following ideas. The weakest families were all attempts to fight the Coinbase move or use a broad 24-hour regime as permission to buy short-term dips.

What Failed: Fading Spot Panic

Panic fading using Coinbase data lost.

- Fade negative Coinbase 15m panic by buying YES: 0 of 5 profitable, mean P&L -$1,022

- Fade positive Coinbase 15m panic by buying NO: 0 of 5 profitable, mean P&L -$1,210

So the lesson is not "always fade volatility." At least in this 30-day window, when the external venue was moving hard, the better trade was to respect the move, not fight it.

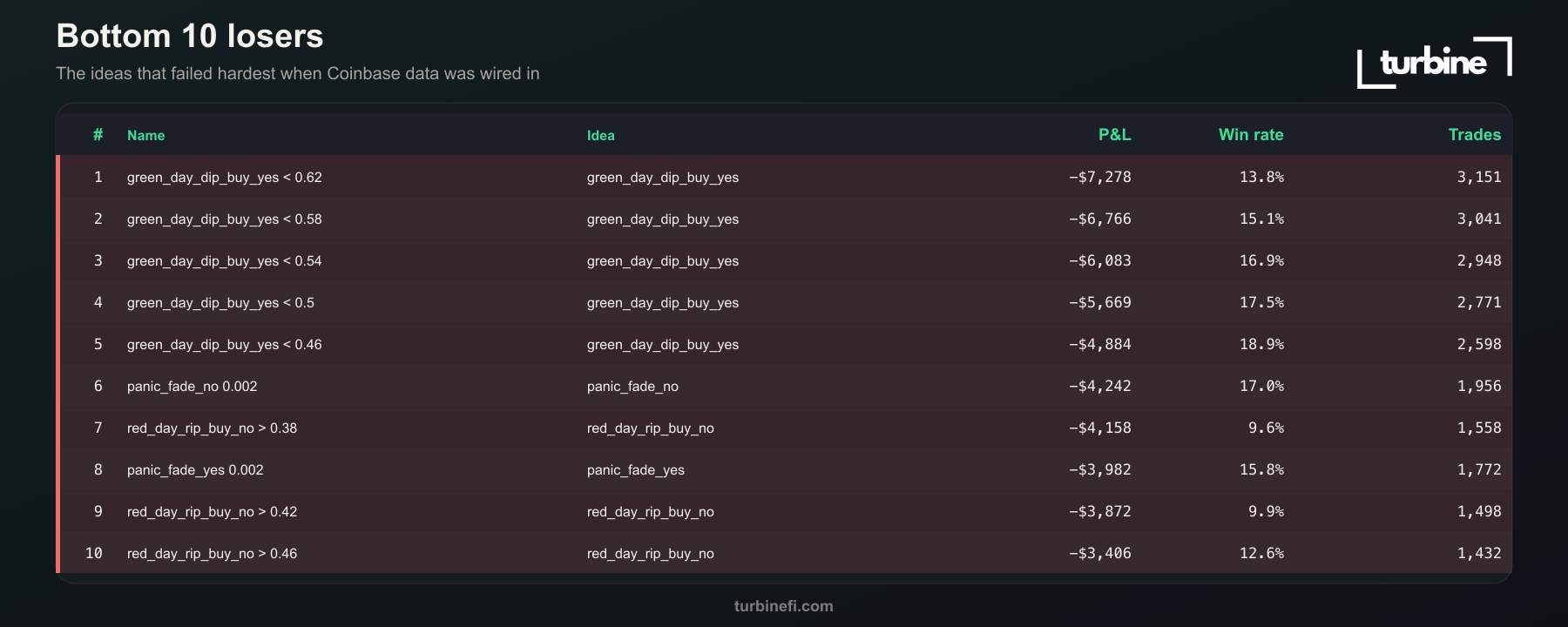

The Real Loser: Regime Dip-Buying

The worst family was green_day_dip_buy_yes.

- 0 of 5 profitable

- Mean P&L: -$6,136

- Worst: -$7,278

The idea sounds reasonable: BTC is in a positive daily regime, so buy short-term dips. It did not work. On 15-minute contracts, the dip was not a bargain. It was usually information.

The matching NO version, red_day_rip_buy_no, also lost: 0 of 5 profitable, with mean P&L -$3,408.

Clean Winners and Clean Losers

The cleanest winning families were velocity, trend alignment, fast moving averages, and micro-momentum. The cleanest losing families were panic fade and daily-regime dip buying.

Bottom Line

What worked:

- 1-minute Coinbase velocity

- 5-minute / 1-hour trend alignment

- Fast moving-average confirmation

- VWAP premium on the YES side

What did not work:

- Fading Coinbase panics

- Buying dips just because the 24-hour regime was green

- Selling rips just because the 24-hour regime was red

This is still one 30-day window and 100 variants. Overfitting is almost certain, and none of this removes regime-change risk. The result we care about is not the exact leaderboard, but the contrast with prior Kalshi-only runs: adding an external signal changed which ideas survived.

The shape is pretty clear: on Kalshi BTC 15-minute markets, the external venue is not just context. It is the lead instrument.

The strongest strategies were not predicting BTC from Kalshi. They were predicting Kalshi from BTC.

How We Ran It

All 100 strategies were generated deterministically, submitted to Turbine's production backtest engine, and run against Kalshi's KXBTC15M market series over the 30-day window ending May 4, 2026.

Each strategy used Coinbase BTC-USD as an external data source. The tested fields included 1-minute velocity, 5-minute change, 15-minute change, 1-hour change, 24-hour change, VWAP, moving averages, highs/lows, and volume.

Signals are evaluated on historical data available at the candle timestamp, with fills no earlier than the next tradable candle. Backtests include modeled fees and slippage, but live execution can be worse.

If you want to run your own version of this, swap the series, change the window, try different external signals. Turbine Studio lets you describe a strategy in plain English, compile it to executable strategy logic, and backtest it before risking capital.

Build a strategy that uses external data.

Caveats

One window (30 days, ending May 4, 2026), one series (KXBTC15M). Different windows can absolutely flip the leaderboard. Treat the shape of the findings as more durable than any individual rank.

We ranked this run by net simulated P&L because all strategies were generated with comparable sizing and risk constraints. High-turnover velocity strategies especially deserve skepticism: they looked dominant here, but they are also the most sensitive to latency, queueing, spread, and venue hiccups.

Backtests use historical orderbook snapshots and historical external data. Live execution hits slippage, venue hiccups, liquidity that moves under you, and operational latency. Past performance, hypothetical or real, does not predict future performance.

Disclaimer

This post is for informational and educational purposes only. It is not investment advice, a recommendation to trade, or a solicitation to buy or sell any financial product, contract, or instrument. Turbine is not a registered investment adviser, broker-dealer, commodity trading advisor, or commodity pool operator.

The results described are from a backtest: a simulation of how strategies would have performed against historical orderbook data over a specific window on a single market series. Kalshi contracts are regulated by the U.S. Commodity Futures Trading Commission.

Hypothetical and simulated performance results have inherent limitations. They are prepared with the benefit of hindsight, do not involve real capital at risk, and cannot fully account for the impact of execution, liquidity, fees, or changes in market conditions. No representation is being made that any strategy will or is likely to achieve profits or losses similar to those shown.

Past performance, whether actual or hypothetical, is not indicative of future results. Trading prediction-market contracts involves substantial risk, including the possible loss of the entire amount invested.

Strategies described here were built and backtested by the author for research. Turbine does not recommend any of these strategies for use.

You are solely responsible for any decisions you make. Before trading any product, consider your financial situation and risk tolerance, and consult a qualified professional. Do not rely on anything in this post as the basis for a trading decision.