How to Trade Kalshi Economic Event Contracts (CPI, Fed, Jobs Reports) in 2026

The Federal Reserve just published research with a surprising finding: Kalshi's modal forecast for the federal funds rate has perfectly matched the realized rate by the day of every FOMC meeting since 2022 (Federal Reserve FEDS 2026-010, Feb 2026). That's a perfect record. Better than Fed funds futures. Better than primary dealer surveys. Better than Bloomberg consensus on inflation prints during shocks.

When the Fed itself starts citing your prediction market as a more accurate forecasting tool than the instruments it built, something has changed. Kalshi processed $22.88 billion in trading volume in 2025 — a 1,100%+ year-over-year jump (Sacra, 2025). Open interest on Fed contracts alone exceeded $450 million as of February 2026 (Wedbush / PredictStreet, Feb 2026).

Here's the practical guide: what economic contracts exist on Kalshi, how to trade them around release days, and where bots are eating the most edge.

**Key Takeaways** - Kalshi's modal Fed funds rate forecast has perfectly predicted every FOMC outcome since 2022 ([Federal Reserve](https://www.federalreserve.gov/econres/feds/files/2026010pap.pdf), 2026) - Open interest on Kalshi Fed contracts exceeded $450M and the platform handled $120B+ in interest-rate market volume this Fed cycle alone - Kalshi prices update in real-time vs. CME FedWatch's 10-minute delay — bots show pre-emptive moves 30 seconds before BLS release pages update - Active arbitrage windows exist between Kalshi, Polymarket, and CME FedWatch when the three diverge by 9-54% on the same event

Why the Federal Reserve Cited Kalshi as a Better Forecaster

The Fed's February 2026 paper "Kalshi and the Rise of Macro Markets" found that Kalshi's headline CPI year-over-year forecasts represent a "statistically significant improvement" over Bloomberg's consensus (Federal Reserve FEDS 2026-010, Feb 2026). On Federal funds rate decisions, the modal Kalshi forecast has matched the realized rate every single time since 2022 — a perfect record.

A separate NBER study examining Kalshi's performance during the 2023-2025 inflation shock period found a 40.1% lower mean absolute error than Bloomberg consensus estimates (Fortune / NBER w34702, Jan 2026). The most useful piece of the Fed paper isn't the headlines — it's the methodology. Researchers measured Kalshi's modal forecast against the actual outcome on FOMC day. Markets converge fast. By the morning of a meeting, Kalshi prices reflect everything traders know.

Why does Kalshi beat traditional forecasting? Three structural advantages. First, real-time pricing — every order updates the market instantly, unlike CME FedWatch which has a 10-minute delay (Kalshi Research, 2026). Second, continuous trading — unlike the NY Fed primary dealer survey which runs on a 6-week cycle. Third, real money — traders are putting capital at risk, not filling out a survey.

**Key insight:** The Fed paper's most useful finding isn't that Kalshi is more accurate — it's that Kalshi's accuracy *converges to perfect* by FOMC day. This means the trading opportunity is in the days *before* the meeting, when the market is still finding price. By the time consensus locks in, the edge is gone. Bot strategies should focus on T-7 to T-1 windows, not the day of the announcement.

For the broader context on how prediction markets are being used, see our breakdown of what prediction markets actually are and why AI agents dominate them.

What Economic Contracts Can You Actually Trade on Kalshi?

Kalshi commands 52.6% of the regulated prediction market by volume (QuantVPS, 2026), and almost all of the macro/economic contract volume in the United States. Here's the menu of what's actively traded:

Federal Reserve Rate Decisions

"Will the Fed raise/hold/cut rates at the next FOMC meeting?" Each FOMC has individual contracts for each possible decision: hold, cut 25 bps, cut 50 bps, hike 25 bps, etc. Peak FOMC contract volume reached approximately 100 million during the September 2025 meeting, with typical recent meetings seeing 1M+ (Federal Reserve FEDS 2026-010, 2026).

CPI and Inflation Contracts

Monthly CPI prints generate active contracts: "Will headline CPI year-over-year exceed 3.0%?" Both headline and core CPI are tradeable. The market-clearing price effectively becomes a real-time consensus number that beats Bloomberg's survey-based forecast during volatile inflation periods.

Nonfarm Payrolls (Jobs Reports)

First Friday of each month at 8:30 AM ET. "Will NFP exceed 200K?" Volumes spike around release windows. Bots show pre-emptive price movements 30 seconds before official BLS website updates (PredictStreet, Jan 2026).

GDP, Unemployment Rate, Jobless Claims

Quarterly GDP prints, monthly unemployment rate, weekly jobless claims. These have lower individual volume than CPI/Fed but produce frequent edge opportunities because they're less covered by retail traders.

Forward-Looking Macro

"Will the Fed cut rates by year-end?" Year-end and multi-meeting contracts let you express longer-duration views. Total trading volume across Kalshi interest-rate markets surpassed $120 billion this Fed cycle alone (PredictStreet, Jan 2026).

How Do Kalshi's Macro Contracts Compare to Fed Funds Futures and TIPS?

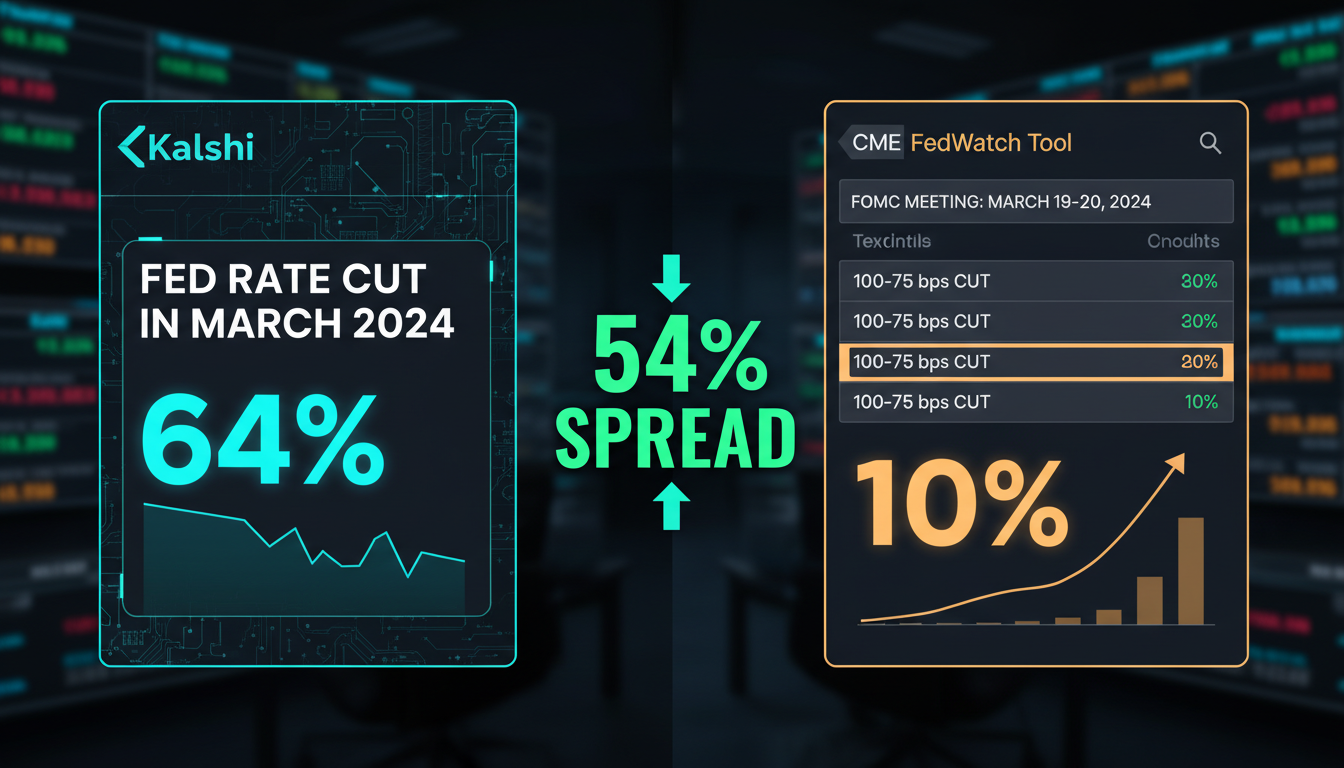

Kalshi prices update in real-time, while CME FedWatch — the standard tool for inferring rate expectations from Fed funds futures — runs on a 10-minute delay (Kalshi Research, 2026). On February 5, 2026, Kalshi traders priced a 64% probability of a March rate cut while CME FedWatch showed only 10% probability of a cut (90% hold) — a 54% spread on the same underlying event (Wedbush / PredictStreet, Feb 2026).

That kind of spread is impossible to ignore. Either Kalshi's wrong, or CME's wrong. Either way, somebody's making money on the convergence.

The Structural Differences That Matter for Traders

Pricing model. Fed funds futures imply rate expectations through a complex calculation involving fed funds settlement prices. Kalshi contracts directly bet on the FOMC decision outcome — no inference needed. Cleaner mental model, faster reaction time.

Liquidity timing. Fed funds futures are most liquid during US futures market hours. Kalshi trades 24/7. When breaking news hits at 2 AM Tokyo time, Kalshi prices move first.

Granularity. Kalshi offers contracts on individual decision outcomes (hold, cut 25, cut 50). Fed funds futures express the average rate, which mixes meeting timing and magnitude. For traders with specific views on a single FOMC, Kalshi is more precise.

Fees. Kalshi charges 7% × p × (1−p) per contract for takers — peaking at $0.0175 per contract at 50¢ pricing (Kalshi Fee Schedule, 2026). Lower than typical sportsbook vig, higher than zero-fee assumptions floating around online. Compared to $1.50-$2.00 per Fed funds futures contract round-trip, Kalshi is cheaper for small trades and more expensive for large ones at the worst-case 50¢ pricing.

For a deeper comparison of platforms, see our Polymarket vs Kalshi guide.

What Does a CPI Release Day Trading Playbook Look Like?

Bots showed pre-emptive price spikes approximately 30 seconds before the official Bureau of Labor Statistics website updates with new CPI data (PredictStreet, Jan 2026). That's not insider trading — it's bots scraping multiple primary sources (lock-up rooms, financial wire feeds, FRED) and reacting milliseconds faster than the BLS public website refresh.

If you're trading manually, this is your cue: you can't beat the bots on speed. You can beat them on conviction.

T-7 Days: Build the Thesis

- Pull recent inflation indicators: gas prices, used cars, OER trend, commodity moves

- Note the Bloomberg consensus number — that's the sportsbook's "line"

- Identify whether Kalshi prices align with consensus or diverge

- If Kalshi is meaningfully different from consensus, ask why

T-1 Hour: Position Sizing

- Reduce position sizes — vol is about to explode

- If your bot is running, verify circuit breakers are armed

- Check Kalshi-Polymarket spread on the same event (typical: 5-15% gap creates arb)

T+0 (Release Moment): Watch, Don't Trade

- The first 60 seconds will see massive price swings

- Bots will overshoot in both directions

- Manual traders who try to react in this window get destroyed

- Wait for the dust to settle before deploying new positions

T+5 Minutes: The Real Opportunity

- Initial reaction is usually overdone

- Mean-reversion plays often work as humans pile in late

- Cross-platform arb between Kalshi and Polymarket peaks here

**From our experience:** The traders who do best on Kalshi economic contracts treat release days like Earth-shattering events for the first 5 minutes and ignore them after. The first move is bots. The second move is humans chasing. The third move — back toward fundamentals — is where systematic strategies print money. Build for T+5 to T+60, not T+0.

How Are Bots Eating Edge in Kalshi Macro Markets?

Trading volume across Kalshi's interest-rate markets surpassed $120 billion in the current Fed cycle, with bot-driven activity accelerating sharply through 2026 (PredictStreet, Jan 2026). The pre-emptive 30-second price spikes before BLS releases — those are bots running scripts to scrape data from multiple sources before the public website updates.

This connects to the broader pattern we covered in our arbitrage bots deep dive. When markets are this efficient at reacting to public data, the edge moves to:

- Better data sources — bots that pull from FRED, BLS API, Fed lock-up wires, and 10+ primary feeds simultaneously

- Cross-platform arb — exploiting the 9% Kalshi-Polymarket spread that typically appears on Fed contracts (PredictStreet, Jan 2026)

- Statistical models — bots running econometric models on leading indicators (gas prices, hiring data, manufacturing PMIs) to generate predictions before consensus

- Strategic position sizing — Kelly Criterion-based bots with multi-meeting forward views

Why Build a Kalshi Macro Trading Bot on Turbine Studio?

Kalshi's free API supports REST, WebSocket, and FIX connectivity for institutional-grade execution. That's the toolkit. The question is whether you want to spend 4-6 weeks building infrastructure (auth, order management, risk controls, hosting, error recovery) or skip straight to strategy.

The hardest part of trading economic contracts isn't writing the strategy — it's building the systems that let your strategy run reliably 24/7 without breaking when the API changes, when the network drops, when an edge case fires.

**Our finding:** Across Turbine Studio users running macro contract strategies, the most successful share three patterns: (1) they trade Fed and CPI contracts but avoid jobs reports (too volatile, too bot-saturated), (2) they take positions T-3 to T-1 days before release, never T+0, (3) they cap exposure at 2-4% of bankroll per contract using fractional Kelly sizing. The least successful try to react to data releases in real time.

Build your first macro contract trading bot on Turbine Studio

If you're new to building bots, our hard way vs. easy way guide breaks down what's actually involved.

Frequently Asked Questions

Are Kalshi economic contracts legal in all 50 states?

Yes for most users. Kalshi operates as a CFTC-designated contract market (DCM), making economic event contracts federally regulated under the Commodity Exchange Act. Federal preemption applies, though some states have challenged sports event contracts specifically. Economic contracts have not faced the same state-level pushback (Kalshi News, 2025).

How much capital do you need to start trading economic contracts?

Kalshi has no minimum deposit. Contracts trade at fractional dollar amounts ($0.01-$0.99). With $500 you can take meaningful positions across multiple FOMC meetings, CPI prints, and jobs reports. Kalshi processed $22.88 billion in 2025 volume across 1.2 million active traders (Sacra, 2025), so liquidity is rarely an issue on major events.

Do bots have an unfair advantage in economic contracts?

For real-time reaction trading, yes — bots show pre-emptive price moves 30 seconds before BLS data updates (PredictStreet, Jan 2026). But manual traders can compete on multi-day positioning, thesis development, and post-release mean-reversion plays. The edge isn't speed — it's framework.

What are Kalshi's actual fees on economic contracts?

Kalshi charges 7% × p × (1−p) per contract for takers, peaking at approximately $0.0175 per contract at 50¢ pricing and approaching zero at extreme prices ($0.01 or $0.99) (Kalshi Fee Schedule, 2026). Compared to Fed funds futures round-trip costs of $1.50-$2.00 per contract, Kalshi is significantly cheaper for retail-sized positions.

Can you arbitrage Kalshi against Polymarket on Fed contracts?

Yes. Kalshi-Polymarket spreads of 9% on rate cut probabilities are typical, with windows lasting 2-7 seconds for the most efficient bots (PredictStreet, Jan 2026). Manual cross-platform arb is impractical given speed requirements, but automated systems consistently capture profits from these gaps.

Macro Markets Are the Most Underexploited Opportunity in Prediction Trading

The Federal Reserve published research saying Kalshi beats traditional macro forecasting tools. The Fed. The Federal Reserve. That's not a hype article on Twitter — that's the central bank essentially confirming that retail traders, bots, and prediction-market makers collectively price macro events more accurately than the markets the Fed itself built to forecast them.

- Kalshi's modal Fed funds rate forecast has perfectly matched every FOMC outcome since 2022

- Open interest on Fed contracts exceeded $450 million in early 2026

- $120 billion+ in interest-rate market volume traded this Fed cycle alone

- Cross-platform arbitrage windows (Kalshi vs. CME vs. Polymarket) regularly hit 9-54% spreads

- Real-time pricing beats CME FedWatch's 10-minute delay every single time

Macro contracts are a smaller share of total prediction market volume than sports, but the edge per dollar deployed is dramatically higher. Sports markets are saturated with bettors and bots. Economic contracts still have rich pricing inefficiencies waiting to be captured.

Start building your first Kalshi macro bot on Turbine Studio and check our guide to strategies you can automate today for inspiration.

This post is for informational purposes only and does not constitute financial, legal, or tax advice. Prediction market trading involves risk of loss, including total loss of invested capital. Past performance does not indicate future results. Consult a financial advisor for advice specific to your situation.