Prediction Market Arbitrage: How Bots Are Making $40M While You Watch

Researchers at IMDEA Networks Institute analyzed 86 million bets and found something staggering: arbitrage traders extracted roughly $40 million in profits from Polymarket between April 2024 and April 2025 (IMDEA Networks / arXiv, 2025). That's $40 million from pricing inefficiencies alone — no prediction skill required.

And it's getting more concentrated. 14 of the top 20 most profitable wallets on Polymarket's leaderboard are bots (Finance Magnates, 2026). Meanwhile, prediction market volume hit $63.5 billion in 2025, up 4x from $15.8 billion in 2024 (CertiK / Yahoo Finance, 2026). More volume means more arbitrage opportunities. More opportunities mean more money on the table for bots that can grab it.

Here's exactly how they're doing it — and how you can too.

**Key Takeaways** - Arbitrage bots extracted $40M from prediction markets in 12 months, with individual bots earning $150K+ ([IMDEA Networks](https://arxiv.org/abs/2508.03474), 2025) - Three arb strategies dominate: structural (YES+NO < $1), cross-platform (Kalshi vs Polymarket gaps), and statistical (weather/polling model divergence) - Arb windows now last 2.7 seconds on average — manual trading is effectively dead - Kalshi's free API, zero trading fees, and CFTC regulation make it the ideal platform for bot-driven arbitrage

How Much Money Are Prediction Market Arbitrage Bots Actually Making?

Bots with automated strategies average roughly $206,000 in profit with win rates above 85%, while humans running identical strategies capture about $100,000 (Yahoo Finance / CoinDesk, 2026). That's a 2x performance gap — same strategy, different execution speed.

The numbers get wilder at the extremes. One bot executed 8,894 trades on short-term crypto contracts, locking in $150,000 by capturing 1.5% to 3% per trade when YES and NO contracts briefly summed below $1.00 (QuantVPS, 2026). Another turned $313 into $414,000 in a single month trading BTC and ETH 15-minute markets with a 98% win rate.

Why do bots crush humans this badly? Speed, coverage, and discipline. A bot monitors hundreds of markets simultaneously. It executes in milliseconds. It doesn't hesitate, second-guess, or take lunch breaks. When an arb window opens for 2.7 seconds — which is the current average — you're not clicking fast enough. The bot already closed the trade.

**Our finding:** Across Turbine Studio users running arbitrage strategies on Kalshi, the most consistent returns come from structural arb on weather contracts — not the high-profile political markets most traders fixate on. Weather markets have wider spreads, more predictable pricing patterns, and less sophisticated competition.

Only 7-8% of all prediction market wallets consistently generate profits (Finance Magnates, 2026). The rest are liquidity for the bots. So which side do you want to be on?

For context on why automation dominates, see our breakdown of 5 prediction market strategies you can automate today.

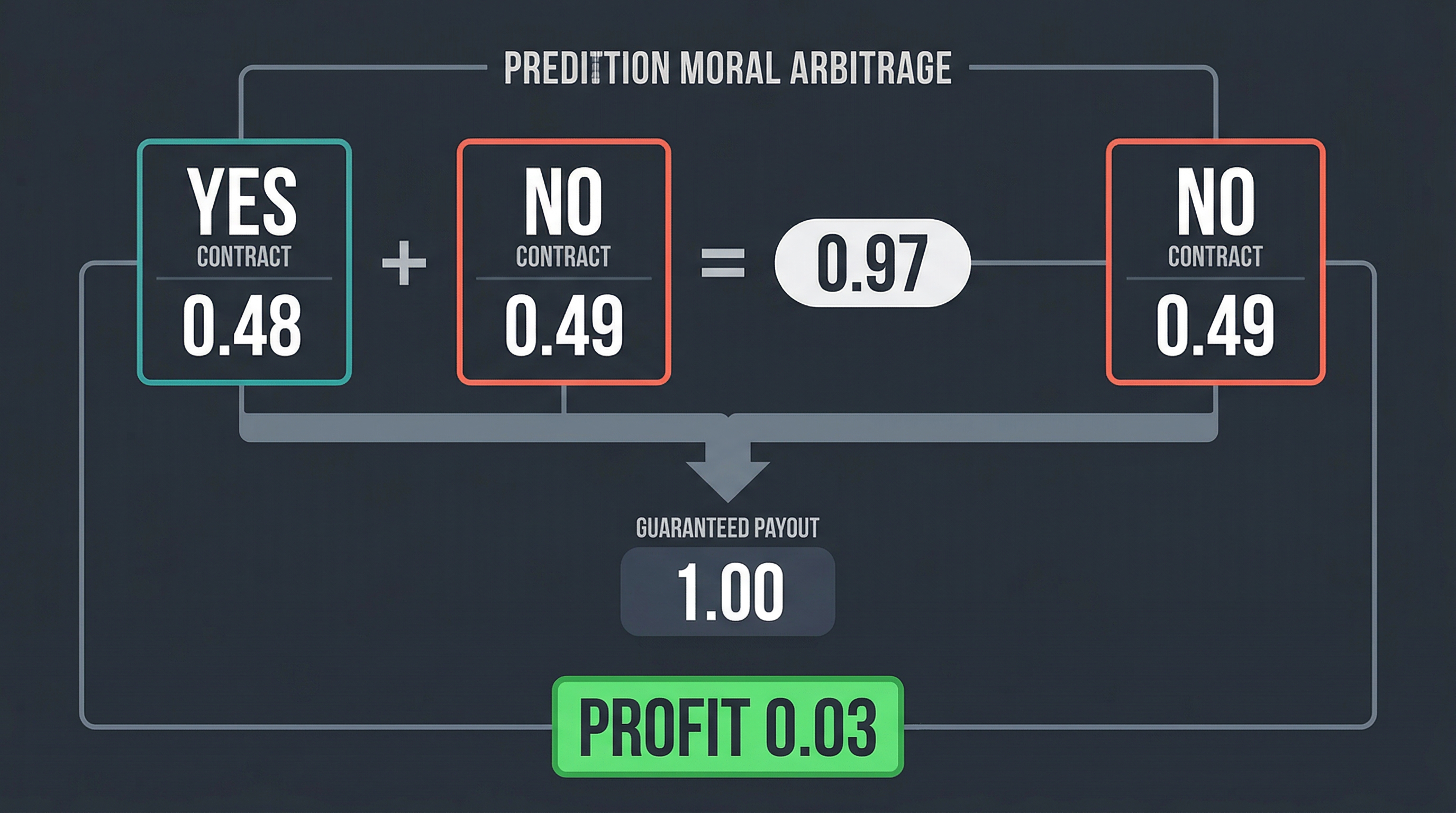

What Is Structural Arbitrage in Prediction Markets?

Every binary prediction market contract has two sides: YES and NO. In a perfectly efficient market, they sum to exactly $1.00. But markets aren't perfect — especially prediction markets, where retail traders push prices based on emotion rather than probability (IMDEA Networks, 2025). When YES + NO drops below $1.00, there may be an apparent arbitrage spread sitting in plain sight.

Here's the mechanic. A contract asks: "Will Bitcoin close above $100K today?" YES trades at $0.48. NO trades at $0.49. Your total cost: $0.97. One side should resolve to $1.00 if the markets settle consistently. The theoretical gross spread is $0.03 per contract before fees, slippage, failed fills, and resolution risk.

Three cents doesn't sound like much. But stack 1,000 contracts and the pre-cost spread is $30. Do that across 50 markets per day and the gross opportunity is $1,500 daily, assuming every leg fills and settles as expected.

Why Speed Matters More Than Anything

The average arbitrage window has compressed from 12.3 seconds in 2024 to just 2.7 seconds in late 2025 (QuantVPS, 2026). That's an 78% reduction in one year. And 73% of all arbitrage profits are now captured by bots executing in under 100 milliseconds.

What does that mean practically? If you're trying to arb manually — opening two browser tabs, checking prices, clicking buttons — the opportunity vanished before you finished reading the prices. Manual arbitrage identification is effectively dead in 2026.

This is exactly why building a trading bot the easy way matters more than ever. The window between "opportunity appears" and "opportunity closes" is now shorter than a human reaction time.

How Does Cross-Platform Arbitrage Work Between Kalshi and Polymarket?

Cross-platform arbitrage between Kalshi and Polymarket yields typical pre-cost spreads of 1.5% to 4.5% per trade, with windows lasting 2 to 7 seconds (AhaSignals, 2026). The concept is simple: the same event is priced differently on two platforms, and you buy opposite sides to capture a possible spread if execution and settlement line up.

Real example from February 2026: the LA Mayoral election was priced at 58 cents for YES on Kalshi and 35 cents for NO on Polymarket. Combined cost: 93 cents. Theoretical gross payout: $1.00 if both venues settled the same way. That's a 7.53% pre-cost spread with execution and resolution risk (Laika Labs, 2026).

BTC hourly markets are the hottest cross-platform arb target right now. Kalshi and Polymarket both offer "Will BTC close above X?" contracts, but their strike prices and odds frequently diverge — sometimes by 5-10 cents. Bots that monitor both platforms via API and execute across both simultaneously are printing money from these gaps.

**Key insight:** Cross-platform arb on prediction markets is structurally different from crypto exchange arb. You're not racing to move assets between venues. You're placing two independent bets on two platforms. Settlement is separate. This means latency is less critical than price monitoring accuracy — making it more accessible for newer bot builders.

For a deeper look at building bots that work across platforms, check our guide to building a Polymarket trading bot.

Statistical Arbitrage: Weather Bots and Model-Driven Trading

Kalshi's KXHIGH weather temperature contracts (covering cities like New York, Chicago, Miami, LA, and Denver) have become a proving ground for statistical arb bots. One documented GitHub bot achieved $1,800 in profits trading these markets using 31-member GFS ensemble forecasts (GitHub / polymarket-kalshi-weather-bot, 2025). Tier 1 Signals, a weather trading signal service, reported 51 wins against just 4 losses on Kalshi weather markets as of March 2026 (Tier1Signals.com, 2026).

Statistical arb works differently than structural arb. Instead of exploiting pricing math (YES + NO < $1), you're exploiting the gap between what the market thinks and what a quantitative model predicts. If NOAA's GFS ensemble says there's an 82% chance Denver hits 90 degrees tomorrow, but Kalshi's YES contract is priced at 68 cents, you've found edge.

The best weather bots run every trade through a multi-model ensemble — combining physical models (GFS, NAM, HRRR) with AI-powered forecasts (AIGEFS). They require edge thresholds above 8% before placing a trade, and cap positions at 5% of bankroll via fractional Kelly criterion (typically 0.25x) to survive losing streaks.

**From our experience:** Weather markets on Kalshi offer something rare — genuine informational asymmetry. Most retail traders are guessing at weather. A bot plugged into NOAA's probabilistic forecast data has a structural advantage that doesn't go away, because most participants aren't running weather models. This edge is more durable than political or crypto arb.

Statistical arb extends beyond weather. Election markets diverge from polling aggregates. Economic data contracts diverge from leading indicators. Any market where a quantitative model can estimate probability better than the crowd is a statistical arb opportunity.

Why Is Kalshi the Best Platform for Prediction Market Arbitrage?

Kalshi processed $23.8 billion in trading volume in 2025 — a 1,108% year-over-year increase — with 97 million trades across 1.2 million active traders (Sacra / HTX Insights, 2026). It's not just the biggest regulated prediction market. It's specifically built for the kind of systematic, API-driven trading that arb strategies require.

Here's why Kalshi stands out for bot builders:

Free API access. Every verified user gets full API access at no cost. REST API, WebSocket streams, FIX connectivity for institutional-grade execution, and official SDKs in multiple languages. No API subscription fees, no rate limit premiums.

Published exchange fees. Kalshi publishes explicit trading fees, so arb bots can model fees before placing orders. For arb strategies where you're capturing 1.5-3% per trade, fees are the difference between profitable and unprofitable.

CFTC regulated. Kalshi is a CFTC-designated contract market (DCM). Your funds sit in segregated accounts at regulated banks. Unlike offshore crypto prediction markets, there's no counterparty risk and no worry about platform solvency. When your bot is running 24/7 with real capital, regulatory protection matters.

Demo environment. Kalshi offers a full sandbox for testing strategies with paper money before going live. You can validate your bot's logic against real market data without risking capital.

Kalshi's $22 billion valuation (as of March 2026) and $260 million in 2025 revenue tell the institutional story: this platform isn't going anywhere (TechCrunch, 2025). When you build a bot on Kalshi, you're building on the most well-capitalized, fastest-growing prediction market infrastructure in the world.

How Do You Build Your First Prediction Market Arbitrage Bot?

Monthly prediction market volume grew from $1.2 billion in early 2025 to over $20 billion in January 2026 (TRM Labs, 2026). The opportunity is growing faster than competition can absorb it. But building a bot from scratch — API integration, order management, risk controls, hosting — takes weeks of engineering work.

Here's the realistic breakdown of what's involved:

The Hard Way (Code It Yourself)

- API integration — Connect to Kalshi's REST API and WebSocket feeds. Parse orderbook data, monitor prices across target markets.

- Strategy logic — Define your arb detection rules. Structural: monitor YES+NO sums. Cross-platform: compare prices across venues. Statistical: plug in model predictions.

- Order management — Place limit orders, handle partial fills, manage positions across contracts.

- Risk controls — Position sizing (Kelly criterion), maximum exposure limits, drawdown circuit breakers.

- Infrastructure — Host the bot on a VPS close to exchange servers. Handle reconnections, error recovery, logging.

This works. But it takes 2-4 weeks of dedicated development, and every bug is a potential loss.

The Easy Way (Turbine Studio)

Describe your arbitrage strategy in plain English. Turbine Studio's AI generates the code, handles the infrastructure, and runs your bot 24/7 on Kalshi. You go from idea to live trading in minutes, not weeks.

Whether you're targeting structural arb on weather contracts, cross-platform gaps between Kalshi and Polymarket, or statistical edges from NOAA weather data — Studio handles the execution layer so you can focus on strategy.

Start building your first arbitrage bot on Turbine Studio

Frequently Asked Questions

Is prediction market arbitrage legal?

Yes, on regulated platforms. Kalshi is a CFTC-designated contract market, making arbitrage trading fully legal for US residents. Polymarket operates offshore and faces different regulatory considerations. The IMDEA study documented $40M in arb profits without flagging legal issues (IMDEA Networks, 2025). Always verify platform terms of service.

How much capital do you need to start arbitrage trading?

Most structural arb opportunities yield 1.5-3% per trade (QuantVPS, 2026). With $1,000 in starting capital and 10 successful arb trades per day at 2% average return, you'd generate roughly $200 daily. Some documented bots started with as little as $313 and scaled from there. Start small, validate your strategy, then increase capital.

Can you do prediction market arbitrage without a bot?

Technically yes, practically no. Average arb windows compressed to 2.7 seconds in late 2025, and 73% of profits go to sub-100ms bots (QuantVPS, 2026). Manual traders can't compete on speed. If you're not automated, you're leaving money on the table — or worse, you're the liquidity that bots are profiting from.

What's the biggest risk in prediction market arbitrage?

Execution risk — one leg fills and the other doesn't, leaving you with directional exposure instead of a hedged position. On cross-platform arb, settlement timing differences can also create temporary capital lockup. Using fractional Kelly sizing (0.25x) and position caps at 5% of bankroll, as documented in successful weather bots (GitHub, 2025), mitigates both risks.

Which prediction market categories have the most arbitrage opportunities?

Weather contracts (Kalshi KXHIGH series), short-term crypto price markets (BTC/ETH hourly), and high-profile political events generate the most consistent arb windows. Weather markets tend to have wider spreads and less sophisticated competition. Crypto markets move fastest but have the most bot competition. Political markets spike around debates and elections.

The Window Is Narrowing — But It's Still Wide Open

Prediction market arbitrage isn't a secret anymore. The $40 million IMDEA study made that clear. But the market is growing faster than competition can fill it. Volume went from $15.8 billion to $63.5 billion in a single year, and it's on pace to exceed $240 billion in 2026.

The traders who build systems now — who automate their arb detection, connect to Kalshi's API, plug into weather models and pricing feeds — are the ones who'll capture the lion's share of profits as these markets mature.

- Structural arb still works, but windows are down to 2.7 seconds. You need a bot.

- Cross-platform arb between Kalshi and Polymarket offers 1.5-4.5% per trade.

- Statistical arb on weather contracts is the least competitive and most consistent.

- Kalshi's free API and published fee schedule make it strong infrastructure for arb bots.

The second-best time to start automating your prediction market trading is now. Build your first strategy on Turbine Studio.

This post is for informational purposes only and does not constitute financial advice. Prediction market trading involves risk of loss, including total loss of invested capital. Past performance does not indicate future results.